Yes. A payment gateway is software and you do not need a banking licence to make your own. You do need to establish acquiring relationships with banks or processors that hold the relevant licences, and you need to comply with PCI DSS to process card transactions securely. Many PSPs and payment businesses operate their own gateways under this model. The acquiring bank handles the financial settlement process. Your gateway handles the routing, security, and customer-facing transaction flow. Any business that can demonstrate a compliant technical setup and a credible commercial model can establish the bank relationships needed to process live transactions.

How to Make Your Own Payment Gateway: Step-by-Step Guide

Making your own payment gateway is one of the most commercially powerful moves a payment business can make. You control the transaction flow, own the customer data, set your own fees, and build a payment product on your terms. This guide explains how to make your own gateway, what it actually involves, what custom decisions you will face, and how to get your own payment infrastructure live without burning two years and a million dollars.

06.05.2026

Why Make Your Own

Payment Gateway

Most businesses that process payments rely on third-party gateways, and pay for that reliance every month. Per-transaction fees, limited routing control, a provider’s brand on your customer checkout, and restrictions on which payment methods you can offer. These are the ongoing costs of not owning your own payment infrastructure.

Making your own payment gateway flips that model. Your gateway processes every transaction your business handles or that your merchants send you. You set the fees. You configure the routing. Your brand appears at your customer’s checkout. Your business owns the payment data.

The case for building your own gateway is strongest for businesses at scale. When your monthly transaction volume reaches a level where per-transaction fees from a third-party provider exceed the cost of running your own gateway, making the switch becomes financially obvious. But the commercial case also applies at smaller scale, particularly for businesses that want to offer payment processing services to other merchants.

When Making Your Own Gateway Makes Sense

PSPs that want to offer branded payment processing to merchants. Banks extending digital payment services to business clients. iGaming operators that need custom routing and multi-provider redundancy. E-commerce platforms that want checkout control and transaction data ownership. SaaS companies that want to add a payment revenue stream. Any business that processes high transaction volumes and wants to stop paying per-transaction fees to a third-party gateway.

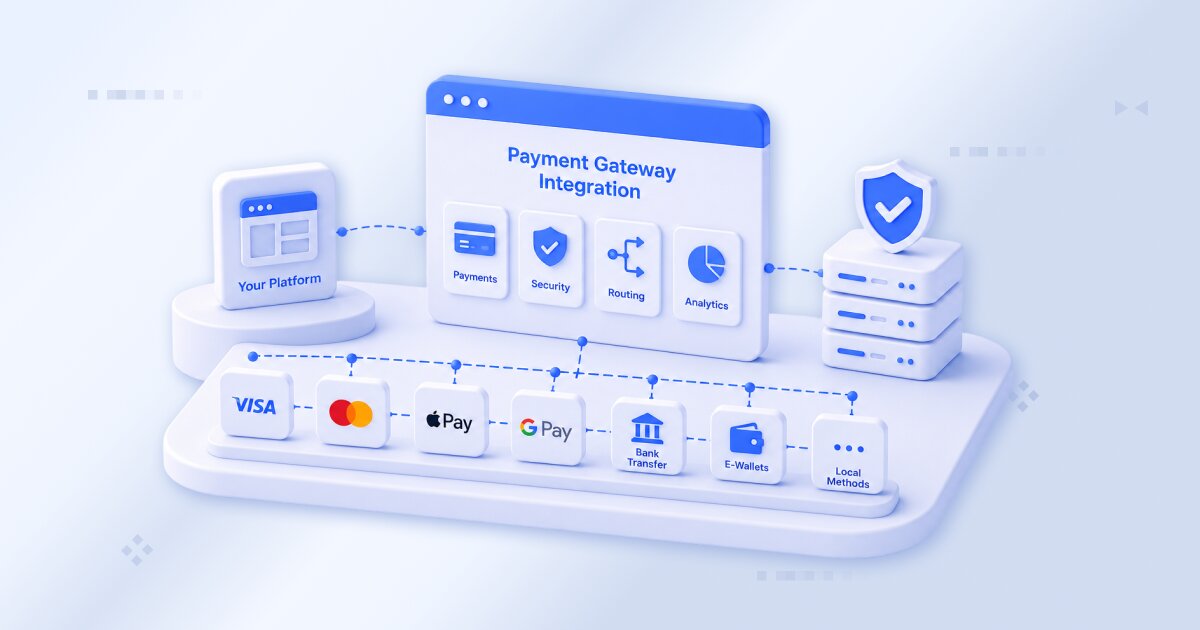

What Your Own Payment Gateway Actually Does

Before you make your own payment gateway, it helps to be precise about what a gateway actually does. Many people conflate a payment gateway with a payment processor or an acquirer. These are different things, and understanding the distinction shapes how you design your own system.

A payment gateway is software. It captures payment data from your customer’s checkout, encrypts and transmits that data to the payment processor or acquiring bank, receives the authorisation response, and returns a success or decline message. The gateway does not hold funds. It does not process the financial transaction itself. It is the secure communication and routing layer between your customer, your merchant system, and the financial network.

Component

Payment Gateway

Payment Processor

Acquiring Bank

Issuing Bank

Card Network

What It Does

Captures, encrypts, and routes transaction data. Returns authorisation responses. Your own gateway is this layer.

Handles technical communication with card networks (Visa, Mastercard) and issuing banks. Connected to your gateway.

Merchant's bank. Receives funds on behalf of merchants. Your gateway connects to one or more acquirers.

Customer's bank. Approves or declines the transaction. Your gateway receives the response.

Visa, Mastercard, Amex, the rules and infrastructure that connect acquirers and issuers. Your gateway operates within these rules.

Payment Gateway

What It Does

Captures, encrypts, and routes transaction data. Returns authorisation responses. Your own gateway is this layer.

Payment Processor

What It Does

Handles technical communication with card networks (Visa, Mastercard) and issuing banks. Connected to your gateway.

Acquiring Bank

What It Does

Merchant's bank. Receives funds on behalf of merchants. Your gateway connects to one or more acquirers.

Issuing Bank

What It Does

Customer's bank. Approves or declines the transaction. Your gateway receives the response.

Card Network

What It Does

Visa, Mastercard, Amex, the rules and infrastructure that connect acquirers and issuers. Your gateway operates within these rules.

When you make your own payment gateway, you are building the software that sits at the centre of this chain. Your gateway processes card data securely, makes smart routing decisions on each transaction, and connects your business to the financial infrastructure that moves money.

How a Custom Payment Transaction Flows Through Your Own Gateway

Here is how a payment transaction flows when your customer pays through your own custom gateway:

01 Customer initiates payment

Your customer enters card data at your custom checkout. Your gateway captures and encrypts the data using TLS. No raw card data travels unencrypted.

02 Your gateway processes the request

Your own gateway applies custom routing rules, selecting the acquirer or payment provider most likely to approve the transaction based on card type, currency, and geography.

03 Authorisation request to the acquirer

Your gateway sends encrypted transaction data to the selected acquirer. The acquirer forwards the authorisation request through the card network to the customer’s issuing bank.

04 Issuing bank responds

The customer’s bank approves or declines. The response travels back through the card network to your acquirer and your custom gateway, typically within 2–3 seconds.

05 Your gateway returns the result

Your gateway receives the response and returns a success or decline to your checkout page. Approved transactions are queued for settlement. Your cascade logic retries declined transactions through backup providers if configured.

06 Settlement

Approved transactions are batched and settled. Funds move through the card network to your acquirer and into the merchant’s account. Your reporting dashboard records every step.

Key Decisions Before You Start Making Your Own Payment Gateway

Making your own payment gateway requires a set of foundational decisions before any development begins. These decisions determine your architecture, your compliance requirements, and your time to market.

Infrastructure model

Will your own gateway run on dedicated servers you control, or on shared cloud infrastructure? Dedicated servers give you more control over your custom payment environment and data residency. Cloud infrastructure scales more easily but requires careful security configuration.

Markets and payment methods

Which geographies will your gateway serve? Which payment methods, card processing, local APMs, digital wallets, crypto, must your own gateway support from launch? Each market has different compliance requirements and customer payment preferences.

Compliance scope

Your own payment gateway must be PCI DSS compliant. The level of certification required depends on your transaction volume. Level 1 is mandatory for gateways processing more than 6 million card transactions per year. Custom gateway deployments typically target Level 1 from the start.

Commercial model

Are you making your own gateway to process your own transactions, or to offer payment processing services to merchants? The commercial model determines your pricing structure, your merchant management requirements, and your onboarding process.

Routing strategy

Your own gateway’s routing logic determines which provider handles each transaction. Custom routing rules, based on card type, currency, approval history, and cost, are what separate a professional payment gateway from a basic payment form.

Fraud and AML approach

How will your custom gateway screen transactions? Rule-based antifraud systems are standard. AI-driven scoring is increasingly common. AML and KYC requirements depend on your jurisdiction and merchant categories.

Thinking about making your own payment gateway?

PayAdmit deploys custom white label gateways in 1–2 weeks. Talk to our team before you start building

Core Components of Your Own

Payment Gateway

Every custom payment gateway, regardless of how you build it, has the same core technical components. Understanding what each component does helps you make better decisions about what to build, what to buy, and what to configure.

1. Payment API Layer

Your gateway’s API is the interface through which merchants, checkout pages, and mobile apps submit payment requests. A well-designed custom payment API handles card transactions, refund requests, recurring billing, and webhook notifications. API-first architecture means any web platform can connect to your gateway through a single integration.

2. Encryption and Tokenisation

Card data captured by your gateway must be encrypted immediately. Tokenisation replaces the raw card number with a non-sensitive token, stored securely in your vault, so your own system never retains customer card data in a usable form. This is the foundational security layer of any compliant custom payment gateway.

3. Transaction Routing Engine

The routing engine is where your own gateway earns its keep. Custom routing rules direct each transaction to the provider most likely to approve it at the lowest cost. Cascading logic retries failed transactions automatically through backup providers. Smart routing in your own gateway can improve approval ratios by 5–15 percentage points compared to single-provider setups.

4. Fraud and Risk Module

Your own payment gateway needs configurable fraud screening. Rule-based systems check transaction parameters against defined thresholds. AI-driven scoring systems analyse patterns across your transaction history to identify suspicious behaviour. The fraud module protects your business, your merchants, and your customers.

5. Merchant Management System

If your gateway processes payments for multiple merchants, you need a merchant management system, a back-office interface where you onboard merchants, configure their payment settings, manage their transaction history, and generate reports. This is where your custom gateway becomes a payment business product.

6. Reporting and Settlement Dashboard

Your own gateway generates enormous amounts of transaction data. A custom reporting dashboard makes that data accessible, real-time transaction monitoring, approval ratios by provider, settlement reconciliation, and custom reports by merchant, currency, or payment method.

Custom Security: How to Make Your Payment Gateway PCI DSS Compliant

Security is not optional when you make your own payment gateway, it is a legal and commercial requirement. Any custom gateway that processes, stores, or transmits card data must comply with PCI DSS. The Payment Card Industry Data Security Standard defines the security controls your gateway must implement and maintain.

PCI DSS Requirement

Network Security

Cardholder Data Protection

Vulnerability Management

Access Control

Monitoring and Testing

Security Policies

What It Means for

Your Custom Gateway

Your Custom Gateway

Your gateway must operate within a protected network environment. Firewalls, network segmentation, and access controls must be configured and documented.

Card data must be encrypted at rest and in transit. Raw card numbers cannot be stored. Tokenisation is the standard approach.

Your custom gateway software must be regularly scanned for vulnerabilities. Security patches must be applied promptly.

Access to card data must be restricted to those who need it. Multi-factor authentication, role-based permissions, and audit trails are required.

All access to cardholder data and network resources must be logged and monitored. Regular penetration testing is required.

Your business must maintain documented information security policies covering all aspects of your custom payment gateway operation.

Network Security

What It Means for

<br>Your Custom Gateway

Your gateway must operate within a protected network environment. Firewalls, network segmentation, and access controls must be configured and documented.

Cardholder Data Protection

What It Means for

<br>Your Custom Gateway

Card data must be encrypted at rest and in transit. Raw card numbers cannot be stored. Tokenisation is the standard approach.

Vulnerability Management

What It Means for

<br>Your Custom Gateway

Your custom gateway software must be regularly scanned for vulnerabilities. Security patches must be applied promptly.

Access Control

What It Means for

<br>Your Custom Gateway

Access to card data must be restricted to those who need it. Multi-factor authentication, role-based permissions, and audit trails are required.

Monitoring and Testing

What It Means for

<br>Your Custom Gateway

All access to cardholder data and network resources must be logged and monitored. Regular penetration testing is required.

Security Policies

What It Means for

<br>Your Custom Gateway

Your business must maintain documented information security policies covering all aspects of your custom payment gateway operation.

PCI DSS Level 1 certification, required for gateways processing over 6 million card transactions annually, involves an annual audit by a Qualified Security Assessor and quarterly network scans. Building your own gateway on pre-certified infrastructure eliminates much of this compliance overhead.

The Compliance Reality

PCI DSS certification is not a one-time process. Your own gateway must maintain certification annually, respond to security incidents, and adapt to updated standards as they are published. Plan for ongoing compliance costs when you make your own payment gateway, not just the initial certification.

How to Handle Card Processing in Your Own Gateway

Card processing is the most technically demanding aspect of making your own payment gateway. To process Visa and Mastercard transactions through your custom gateway, your business must establish acquiring relationships, comply with card scheme rules, and implement the technical protocols required by each network.

Establishing Acquiring Relationships

Your own gateway needs at least one acquiring bank relationship to process card transactions. Acquirers approve merchants and provide access to the card networks. Most custom payment gateways connect to multiple acquirers, enabling smart routing and providing redundancy if one acquirer experiences issues. Building your own multi-acquirer setup gives your gateway significant routing flexibility.

Card Scheme Rules and Compliance

Every custom gateway that processes card payments must comply with Visa and Mastercard operating rules. These rules govern how card data is handled, how disputes are managed, how transactions are formatted, and how your gateway presents itself to customers. Non-compliance can result in fines, transaction suspension, or loss of processing rights.

3D Secure 2 Authentication

3DS2 is now mandatory for most card-not-present transactions in Europe and increasingly required in other markets. Your own payment gateway must implement 3DS2 to perform strong customer authentication. This reduces fraud liability and in most cases improves payment approval rates for legitimate customers.

Recurring Billing and Tokenisation

If your custom gateway processes subscription payments or stored card transactions, you need a tokenisation system. Customer card data is captured once, replaced with a token stored in your vault, and used for all subsequent transactions. Your customers can pay repeatedly without re-entering card details, and your gateway never stores raw card data after the initial capture.

Building from Scratch vs. White Label: Two Ways to Make Your Own Payment Gateway

When you decide to make your own payment gateway, there are fundamentally two paths. Both result in a gateway you own and operate under your own brand. The differences are in cost, speed, and the amount of custom development work required.

Factor

Time to your own live gateway

Development cost

PCI DSS for your gateway

Custom payment methods

Your own branding

Transaction data ownership

Ongoing maintenance

Build from Scratch

12–24 months

$500K–$1.5M+

Separate programme,

6–12 months

Each requires separate integration

Fully custom design

Full

Your in-house team

White Label Gateway

1–4 weeks

Fraction of custom build

Included with provider

400+ pre-built, ready for your gateway

Your domain, your brand

Full

Provider handles it

Time to your own live gateway

Build from Scratch

12–24 months

White Label Gateway

1–4 weeks

Development cost

Build from Scratch

$500K–$1.5M+

White Label Gateway

Fraction of custom build

PCI DSS for your gateway

Build from Scratch

Separate programme,

6–12 months

White Label Gateway

Included with provider

Custom payment methods

Build from Scratch

Each requires separate integration

White Label Gateway

400+ pre-built, ready for your gateway

Your own branding

Build from Scratch

Fully custom design

White Label Gateway

Your domain, your brand

Transaction data ownership

Build from Scratch

Full

White Label Gateway

Full

Ongoing maintenance

Build from Scratch

Your in-house team

White Label Gateway

Provider handles it

The white label approach does not mean you are renting someone else’s gateway. You own and operate the product. Your customers and merchants interact only with your brand. The difference is that the technical infrastructure, the code, the certifications, the integrations, is pre-built. You configure it, brand it, and run it as your own.

The Commercial Logic

For most businesses making their own payment gateway in 2026, building from scratch is not commercially viable unless you have a very specific custom requirement that no existing platform can meet. The white label path gives you full ownership at a timeline and cost that lets you focus resources on merchant acquisition and business growth.

How Long Does It Take to Make a Payment Gateway

The timeline for making your own payment gateway varies

significantly depending on the approach you take.

Approach

Full custom build from scratch

White label gateway (your own domain)

Cashier service (shared infrastructure)

Payment Bridge middleware

Realistic Timeline

12–24 months for an MVP. 18+ months for a production-grade gateway with full card processing and compliance.

1–4 weeks to a live, production-ready custom gateway. PayAdmit deploys in 1–2 weeks.

Days to a custom branded checkout with full payment method coverage.

14 days to connect your existing systems to 400+ payment methods.

Full custom build from scratch

Realistic Timeline

12–24 months for an MVP. 18+ months for a production-grade gateway with full card processing and compliance.

White label gateway (your own domain)

Realistic Timeline

1–4 weeks to a live, production-ready custom gateway. PayAdmit deploys in 1–2 weeks.

Cashier service (shared infrastructure)

Realistic Timeline

Days to a custom branded checkout with full payment method coverage.

Payment Bridge middleware

Realistic Timeline

14 days to connect your existing systems to 400+ payment methods.

The biggest variables in any custom payment gateway project are PCI DSS certification (6–12 months if done independently), acquiring bank relationships (weeks to months to establish), and payment method integrations (each individual integration adds 2–8 weeks). A white label approach handles all three simultaneously.

Custom Payment Gateway for Different Business Types

How you make your own payment gateway, and what custom features matter most, depends significantly on your business model. Here is how gateway requirements differ across the industries PayAdmit serves:

PSPs and Payment Providers

When a PSP makes its own payment gateway, the primary requirement is a merchant management system that handles onboarding, transaction reporting, and individual merchant routing configurations. Your gateway becomes your core product, the thing you sell to merchants. Custom branding, custom pricing per merchant, and the ability to manage hundreds of merchant accounts from a single dashboard are essential.

White Label Payment Gateway for PSP

iGaming and Online Gaming Operators

iGaming operators need custom payment gateways that handle high transaction volumes, process payments across multiple currencies, and manage chargebacks at scale. Smart routing between multiple acquirers is critical, approval ratios directly impact player conversion. Your gateway must also embed AML compliance workflows, as gaming transactions attract regulatory scrutiny.

White Label Payment Gateway for iGaming

Banks and Financial Institutions

Banks making their own payment gateway typically need to extend digital payment capabilities to business customers. Your custom gateway must integrate with existing core banking systems, comply with banking-grade security requirements, and provide the same reliability levels customers expect from traditional financial services.

White Label Payment Gateway for Banks

E-commerce and Marketplace Platforms

E-commerce businesses need custom gateways that manage split payments across multiple merchants, automate settlement payouts, and handle returns and refunds efficiently. Your gateway’s customer checkout experience directly impacts conversion rates, custom payment page design matters as much as technical performance.

White Label Payment Gateway for eCommerce

SaaS and Subscription Businesses

SaaS companies making their own payment gateway need robust recurring billing capabilities. Your custom gateway must handle subscription lifecycle management, failed payment retries, dunning management, plan upgrades and downgrades, with the flexibility to support any billing model.

Common Mistakes When Making Your Own Payment Gateway

Having helped businesses make their own payment gateway across dozens of markets, we see the same mistakes repeatedly. Knowing them in advance saves time, money, and significant technical debt.

Underestimating compliance costs

PCI DSS certification for your own gateway is not a one-time project. Annual re-certification, quarterly scans, and the cost of maintaining a compliant custom infrastructure add up. Build ongoing compliance costs into your business model from day one.

Building before establishing acquiring relationships

Your own custom gateway can only process card transactions once you have acquiring bank relationships in place. These relationships take time to establish and often require demonstrating your gateway’s technical capability. Start the acquiring process early.

Integrating payment methods one at a time

Building individual integrations with each payment provider is slow and expensive. Every new market your gateway enters requires new local payment method integrations. Pre-built integration libraries eliminate this bottleneck.

Ignoring customer checkout UX

Your gateway’s technical performance matters, but so does your customer’s checkout experience. A custom payment page that is slow, confusing, or mobile-unfriendly costs you transaction approvals regardless of how well your routing performs.

Single-provider dependency

A custom payment gateway that routes all transactions through one acquirer is vulnerable. Provider downtime, approval ratio drops, or commercial disagreements can take your entire gateway offline. Your own gateway should connect to multiple providers from launch.

No cascade logic

Failed transactions in a single-provider setup stay failed. A custom gateway with cascade logic automatically retries declined transactions through alternative providers, recovering revenue that would otherwise be lost.

PayAdmit: Make Your Own Payment Gateway Without the Build Overhead

PayAdmit is a payment software company that helps businesses make their own payment gateway in 1–2 weeks, not 18 months. Our white label gateway solution gives you full ownership of your payment infrastructure: your domain, your brand, your routing logic, your transaction data, your margins.

We deploy your own custom gateway on dedicated servers, connect it to 400+ payment methods from launch day, and include PCI DSS Level 1 certification as standard. You make all the business decisions, which merchants to onboard, how to route transactions, what fees to charge. We handle the technical infrastructure and keep it running.

What You Own with a PayAdmit Gateway

Your own domain and brand on all payment pages. Dedicated server infrastructure under your control. 400+ pre-integrated payment methods including card processing, Apple Pay, Google Pay, SEPA, local APMs, and crypto. PCI DSS Level 1 certification included. Smart routing and cascading logic configurable from your admin panel. AML, KYC, and antifraud tooling built in. 24/7 support from real payment specialists. All transaction data belongs to your business.

Our team also works with you beyond deployment, helping you optimise your routing, improve your approval ratios, and connect with potential merchants directly. Making your own payment gateway is the starting point. Growing a payment business around it is where the commercial value compounds.

A gateway is only half of the business — for the licensing, banking and go-to-market side, see our full guide on how to create a payment processing company.

Frequently Asked Questions

Can I make my own payment gateway without being a bank?

How much does it cost to make your own payment gateway?

Building a custom gateway from scratch costs $500K to $1.5M and takes 12 to 24 months. That figure covers core development, security architecture, bank integrations, PCI DSS certification, and the infrastructure needed to process customer transactions reliably at scale. Every business that takes this path also carries ongoing maintenance costs of 30 to 40 percent annually. Making your own gateway through a white label platform like PayAdmit costs a fraction of that and deploys in 1 to 2 weeks. Both approaches give you full ownership of the gateway and full control over how you process payments and serve your customers. The difference is how much you pay and how long you wait to get there.

What is the difference between making your own payment gateway and using Stripe?

When you use Stripe, you are a customer of Stripe’s payment infrastructure. Stripe’s brand can appear at your customer checkout, Stripe controls the routing logic, and Stripe charges per-transaction fees that your business cannot negotiate. When you make your own payment gateway, your brand appears at checkout, you control the routing, and you set your own fees. You can process transactions for other merchants and earn on every payment they process through your platform. You own the product rather than renting it. For any business that processes significant transaction volumes or wants to offer payment processing as a service to other businesses, making your own gateway is the commercially superior model.

Can my payment gateway process cards from any country?

Yes, if you have the right acquiring relationships in place. Card processing in different regions requires connections to local acquirers or processors with coverage in those markets. The security requirements, compliance obligations, and customer authentication standards also vary by region, so your gateway needs to handle each market’s specific process correctly. A pre-built integration library covers most global markets and can handle the regional compliance and security differences automatically. Your own gateway can process card transactions in 40 or more markets from launch day, with each market’s customer payment experience handled correctly without additional development work from your side.

How do I handle customer card data securely in my own gateway?

Tokenisation is the standard security approach. When your customer enters card data, your gateway encrypts it immediately and replaces the card number with a token. The token is stored in your vault. Raw card data never persists in your system after the initial secure capture. This security model reduces your PCI DSS scope significantly and protects customer data in the event of a breach because there is no usable card data left to steal. Every business that makes its own payment gateway needs to implement this security layer before processing live customer transactions. Skipping tokenisation means carrying the full PCI DSS security compliance burden for every customer card number your gateway has ever seen.

What is the fastest way to make my own payment gateway?

The fastest path is a white label gateway deployment. Any business that needs its own production gateway quickly can deploy through PayAdmit in 1 to 2 weeks. This includes custom branding, 400 or more payment method connections, PCI DSS certification, routing configuration, security layer setup, and full admin panel configuration. The security and compliance work that can take a custom development project 6 to 12 months is already done. Your business can process customer transactions, onboard merchants, and start earning on every payment from week two. There is no faster commercially viable path to your own production gateway that can handle real customer transactions securely and at scale.

ADDITIONAL RESOURCES

How to Own a Payment Gateway

Owning a payment gateway means more than having a checkout form on your website.

Payment Gateway Integration Services

Payment gateway integration services are the technical and operational work that connects your business systems, your website, app, or platform, to the payment infrastructure that processes transactions.

What Is a White Label Payment Gateway

In plain terms: someone else builds the engine. You put your name on the hood, set the rules, and keep the revenue.