A small business can create a branded payment gateway by deploying a white label solution like PayAdmit rather than building from scratch. Any business, from a small company to a mid-size company running its own payment operations, can deploy a white label payment solution and can be up and running in weeks. The white label approach gives your business dedicated infrastructure, your own PCI DSS environment, full payment routing control, and a branded customer checkout, at a cost and timeline that small and mid-size businesses can actually achieve. Your customer data stays in a dedicated, certified environment. Customer card data never touches shared infrastructure. Your company does not need a compliance team to manage PCI DSS, that is handled on your behalf.

HOW TO CREATE A PAYMENT GATEWAY: REQUIREMENTS, COSTS, AND THE SMARTER ALTERNATIVE

A practical guide to creating a payment gateway: architecture requirements, PCI DSS compliance, real cost breakdown, and how businesses use PayAdmit's white label solution instead.

What Creating a Payment Gateway Actually Involves

Most businesses researching how to create a payment gateway expect a software project. The question of how to create a payment gateway comes up regularly as fintech businesses scale. This guide walks through how to create a payment gateway step by step, from compliance to launch to live transactions.

Operators that have decided on the buy path and want to see the brand-customisation side of the deployment can review the service overview on how to create a payment gateway built for your brand, including custom domain, checkout styling, and merchant-facing branding.

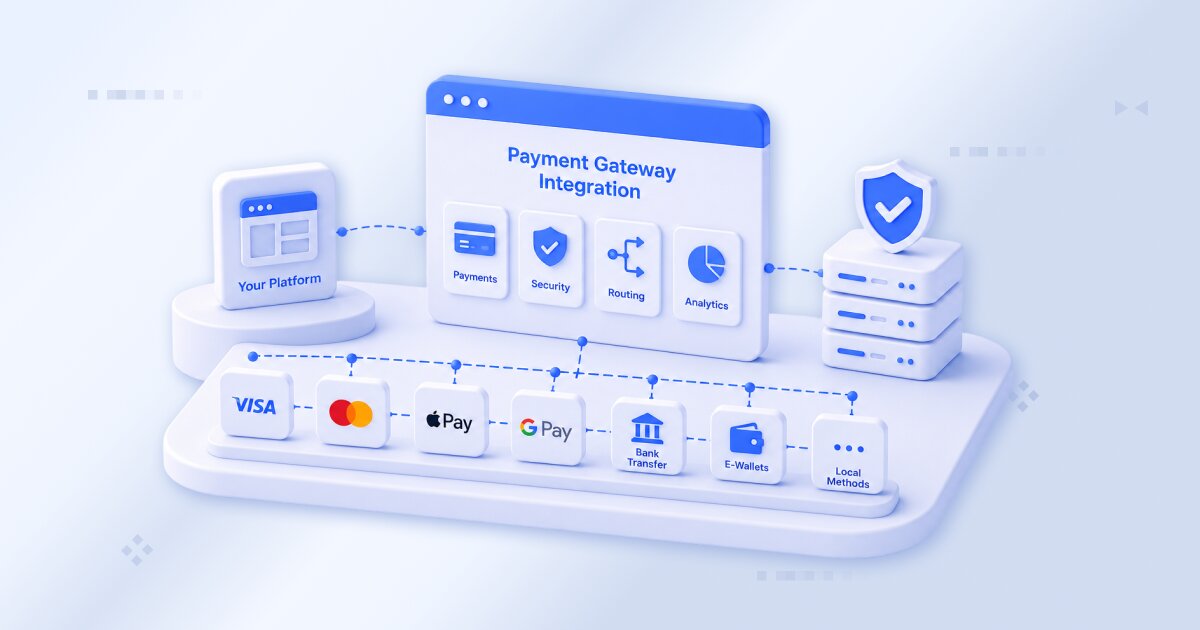

A payment gateway is the system that receives payment data at checkout, validates the payment, encrypts it, routes it to the acquiring bank or payment processor, and returns an authorization response. Every time a buyer enters details on a website or clicks to pay, the payment gateway handles the payment cycle. When it works, the buyer sees a payment confirmation. When it fails, the payment is lost.

The core payment process the gateway must handle includes:

- Capturing payment card data or digital wallet credentials

- Applying payment encryption at the point of capture

- Routing each payment through the correct payment processing path to the PSP or acquiring bank

- Handling declined payment requests, running payment retry processes, and executing payment cascading

- Returning the payment transaction result and payment status to the website in real time

- Logging every payment event for payment settlement, payment reconciliation, and dispute management

Each payment step has security requirements, compliance obligations, and technical dependencies. None of them can cut corners without creating business and legal risk.

Who Should Consider Creating Their Own Payment Gateway

The businesses that justify creating a payment gateway are those where payment processing is the core activity. This does not apply to every business that processes payments. The right answer depends on the business model.

The businesses that justify this investment are PSPs that want direct control over processing infrastructure, fintech businesses that need to embed payment processing natively in their product, and large enterprises with unique requirements that no existing solution meets.

For these businesses, the business case rests on three factors. First, transaction volume: at high business transaction volumes, the per-transaction margin can justify the cost.

Second, product differentiation: if the payment experience is part of the core product, a redirect to an external payment page breaks the product experience. Third, routing control: direct routing control is the only way to achieve that level of optimization when your business needs to manage approval rates across multiple PSPs.

If the business does not fit one of these three profiles, understanding how to build a payment gateway usually reveals that a custom build will cost more than it saves. For most businesses, a white label solution is the better path.

Business Profile Check

Ask three questions before committing to a custom build. Does your business earn revenue directly from payment processing fees? Does your core product require a payment experience that cannot redirect to a third party? Does your business process enough payment volume that routing control affects revenue by a measurable percentage? If the answer to all three is yes, the custom build case is worth exploring. If not, a white label solution delivers the same operational outcome without the build cost.

WHAT THE PAYMENT PROCESS LOOKS LIKE FOR YOUR BUSINESS

Business clients increasingly expect their bank to provide a complete payment solution, card acceptance and payout management, as part of the banking relationship.

The Process Breaks at Scale

A payment process that works for 100 transactions per day needs re-engineering for 100,000. Gateway infrastructure that processes transactions reliably at high volume requires dedicated server infrastructure, distributed processing, real-time failover, and load balancing. Many businesses that create a payment gateway underestimate the gap between a functional prototype and a production-grade payment system. Factor the scale requirement into the architecture from day one.

Before any payment gateway can process a transaction, several payment components must work together. Understanding this payment process helps the business evaluate whether building from scratch or deploying a white label solution makes more sense.

A payment transaction starts when a buyer submits payment details at checkout. The payment gateway runs a payment validation check. The payment information then routes to the correct PSP or acquiring bank based on routing rules the business has configured. The PSP processes the payment and returns an authorization. The payment gateway logs the result and returns the payment status to the merchant.

This payment process sounds simple, but every edge case must be handled. A payment can fail because the card has insufficient funds, it has expired, or the bank flags the transaction as suspicious. The business needs cascading logic so failed payments route to a backup PSP automatically. Real-time reporting lets the business monitor payment authorization rates and PSP performance issues. The same process applies to every payment type and every geography the business operates in.

For most businesses, handling all of this from the ground up is not the right starting point. A white label solution handles the full payment process from day one, businesses connect to live, tested payment infrastructure in weeks. The business can focus on growth, not on the payment process infrastructure.

THE TECHNICAL REQUIREMENTS: WHAT YOUR PAYMENT GATEWAY NEEDS

Payment Data Capture and Encryption

Your gateway must capture payment card data through a secure form on your website or mobile interface. The payment gateway applies payment encryption immediately at capture, skipping this security process is not an option. Payment information must never pass through your servers in plain text. Any gap in this process exposes the business to liability. TLS/SSL encryption is mandatory for all payment data transmission.

Transaction Routing Engine

The routing engine is the intelligence layer of your payment gateway. It decides which PSP or acquiring bank receives each payment, based on card BIN, geography, amount, and live approval rate statistics. A payment gateway with intelligent routing can improve payment approval rates by one to three percentage points compared to a gateway that sends all payment transactions through a single path. At high payment volumes, that approval rate difference is measurable revenue.

PSP Integration and Cascading

Your gateway needs direct API connections to payment processors and acquiring banks. Each PSP integration requires its own development process, testing process, and legal agreement. When a payment fails at the first PSP, the gateway automatically cascades, the process continues to the next configured processor within the same checkout session, without the buyer knowing the first attempt failed. Cascading logic is critical for businesses where a failed payment is lost revenue.

Anti-Fraud and Risk Management

Payment information is a target for fraud. The payment gateway evaluates each payment request before it reaches the acquiring network. This includes velocity controls, BIN checks, behavioral scoring, device fingerprinting, and optional third-party fraud scoring tools. Each layer adds security depth to the payment process. If the business processes payments in multiple geographies, the payment fraud rules need to account for different risk profiles per market.

Settlement, Reconciliation, and Reporting

Your payment gateway must track every payment from authorization through capture, settlement, and payout. The payment settlement process connects payment gateway records with the acquiring bank’s settlement records, this process runs for every payment processed. The reconciliation process identifies payment discrepancies. Without accurate payment settlement and reconciliation, the business cannot manage payment chargebacks or provide merchant businesses with accurate records.

Merchant Portal and API Layer

If your payment gateway serves multiple merchants, each merchant needs a portal to view their payment transaction data, configure their payment settings, and access payment settlement and payment reporting. The gateway also needs a documented REST API that merchants or product teams can use to initiate payments, manage transactions, and access payment data programmatically.

SECURITY AND COMPLIANCE: THE NON-NEGOTIABLE LAYER

Creating a payment gateway without proper security and compliance is not possible. Regulators, card networks, and acquiring banks all require specific security standards before a payment gateway can process customer payment transactions.

PCI DSS Timeline Reality

The PCI DSS certification process includes a server infrastructure review, security architecture analysis, access controls review, encryption methods assessment, and security monitoring systems evaluation. The QSA assessment almost always identifies gaps that require remediation before certification is granted.

Teams that decide to build a payment gateway in-house need to budget not only for the initial engineering work but also for PCI DSS certification, acquirer integrations, fraud screening modules, and a permanent payment engineering team.

WHAT IT COSTS TO CREATE A

PAYMENT GATEWAY

Here is how the payment gateway cost breaks down across the first year, and how costs stack for ongoing operations.

Total Year 1 estimate: $460,000 – $1,240,000

Annual ongoing cost: $150,000 – $300,000

This is a permanent business cost, not a one-time development project. This ongoing cost affects every payment business that builds from scratch. These figures assume the team already has payment engineering experience. Teams reviewing how to develop payment gateway infrastructure end-to-end need a complete picture of the engineering stack, from card capture and tokenisation through to settlement reporting and reconciliation.

WHITE LABEL VS CUSTOM:

THE DECISION FRAMEWORK

Before the business decides how to create a payment gateway, use this framework to evaluate which approach fits the situation.

The key insight from this comparison: both approaches give the same routing control. The ownership model differs, not the operational capability. A custom payment gateway and a white label solution both deliver full payment control.

Businesses that go the custom route typically spend 12 to 24 months and $500,000 to $1,000,000 before processing their first live payment. For most businesses, this is not the right starting point. The white label path gets to the same result faster and at lower cost. The payment process is identical. The business launches with full payment functionality without the compliance timeline.

HOW YOUR BUSINESS CAN CREATE A BRANDED PAYMENT GATEWAY WITH PAYADMIT

PayAdmit provides a white label payment gateway that gives the operator full ownership of the payment experience. Your business gets a live payment gateway without the cost and timeline of creating the payment infrastructure from scratch. You can launch payment processing in weeks, not months. Your customers go through a payment process that feels like your own product, because it is.

Your Own PCI DSS Environment

Each client deployment runs on dedicated server infrastructure with its own PCI DSS certification. Payment information stays in a dedicated environment. Your PCI DSS compliance scope narrows to the dedicated deployment. PCI DSS maintenance, security architecture updates, and card network compliance management are handled by PayAdmit.

Full Transaction Routing Control

The PayAdmit routing engine evaluates each payment by card BIN, geography, amount, PSP approval rate statistics, and merchant risk profile. Routing rules set per deployment. The gateway executes them in real time. When a payment fails at the first PSP, the cascading engine routes to the next configured processor automatically, the buyer sees a seamless payment process.

Your Brand at Every Payment Touchpoint

Payment pages, checkout forms, receipt emails, and merchant portals run on the operator’s domain with the operator’s brand. Third-party brands do not appear in the buyer-facing process. Merchants interact with a payment portal that carries your identity. PayAdmit delivers complete REST API documentation covering all payment operations under your brand, ready for technology partners and merchant integration teams.

400+ Payment Method Integrations on Day One

There is no need to build individual payment PSP integrations. PayAdmit provides access to 400+ card networks, digital wallets, alternative payment methods, and regional processors. When an operator needs a payment method not in the network, PayAdmit’s team handles the integration development within one to two weeks. Any business can deploy a white label payment solution and can be up and running in weeks.

Deployment: What the Process

Looks Like

A branded payment gateway with PayAdmit deploys in two to three weeks. Here is how that deployment works and how each step connects.

Week 1: Infrastructure and Configuration

PayAdmit deploys and maintains the complete infrastructure in 2 to 3 weeks. Dedicated server infrastructure provisions for the deployment. PCI DSS certification activates. Branded checkout pages deploy on the operator’s domain with the operator’s brand on every payment page. Initial PSP connections configure based on routing requirements.

Week 2: Integration and Testing

The integration process covers payment initiation, payment processing, payment webhook configuration for payment events, and merchant account setup. Sandbox testing confirms the payment processing logic. The test process validates the payment flow and payment event delivery. This process must pass before go-live.

Week 2–3: Launch and Ongoing Operations

The branded payment gateway goes live and accepts payment transactions through the operator’s branded interface. Routing configuration, merchant accounts, and settlement reporting manage from the white label back office. The operator manages commercial relationships. PayAdmit manages the payment technical stack, security updates, card network rule changes, PCI DSS renewals, and BIN database updates.

When evaluating alternatives to the full build, the obvious comparison point is what is a white label payment gateway and how the licensed model handles each cost line of the original gateway construction work.

A gateway is one component in a bigger picture — see our broader walkthrough on how to build a payment system for the full architecture view.

For teams evaluating the crypto side of the same question, our companion guide on how to create a crypto payment gateway covers the specific architecture, custody and compliance decisions that only apply to crypto.

See how PayAdmit deploys your complete payment infrastructure in 2 to 3 weeks.

Frequently Asked Questions

How to create a payment gateway for a small business?

How to create your own payment gateway without building from scratch?

The answer to how to create your own payment gateway depends on your technical capacity and your timeline. A white label payment gateway like PayAdmit gives your business all the capabilities of a custom-built gateway, dedicated servers, configurable routing, branded checkout, and your own API documentation, without the build cost or the compliance timeline. Your customer card data processes through a dedicated, certified environment. Customer payment data, customer transaction records, and customer card credentials are all stored and managed within your company’s own infrastructure layer. Most businesses in this space deploy white label solutions rather than building from scratch.

How to create a payment gateway like Stripe?

Stripe is a hosted payment gateway. When businesses say they want something like Stripe, they typically mean they want to offer payment services to merchants under their own brand, which is exactly what a white label payment gateway enables for a company of any size. A white label gateway gives your company branded checkout, merchant management, transaction routing, and a full payment API, without appearing as a third-party payment brand in the customer’s experience. Your customer sees your brand at every step. Customer card data, customer transaction history, and customer payment preferences all sit within your company’s own environment. Stripe keeps customer data on its own infrastructure; your white label gateway keeps that customer data under your company’s control.

Can any company create its own payment gateway?

Any company can create a payment gateway if the team can handle the technical requirements, but not every company can afford the timeline. Technically possible does not mean financially viable. For most companies, the question is not whether they can create a payment gateway, but whether the cost and timeline justify building versus deploying a white label solution that gives the same operational result. A white label solution gives your company the same customer-facing outcome: your brand, your customer data environment, your card processing rules, and your own API. Customer card data processes in your company’s dedicated environment. Data ownership, data compliance, and data security all remain with your company.

What security standards apply when you create a payment gateway?

Any payment gateway that handles customer payment card data must comply with PCI DSS. The PCI DSS process covers server infrastructure, security architecture, access controls, encryption methods, and security monitoring systems. Card network certifications from Visa and Mastercard are required separately. Customer payment card data must meet encryption standards at capture, in transit, and at rest. Customer data privacy regulations including GDPR apply depending on the markets the gateway serves, customer data processing, customer data retention, and customer data transfer rules all apply. AML and KYC obligations may apply depending on the merchant types the gateway onboards.

How does the payment process work in a white label gateway?

The buyer payment process follows the same steps as a custom-built gateway. A customer submits card details on the branded payment checkout. The payment gateway captures customer card credentials, validates the customer’s card data against BIN records and fraud rules, routes the payment transaction to the configured PSP through the payment processing path, receives the payment authorization response, and completes the payment cycle. The payment gateway returns the payment status to the merchant. Customer card data never leaves your dedicated environment. The buyer’s session stays on the operator’s domain. Third-party brands do not appear in the buyer-facing process. Your customer interacts only with your brand, from card entry to payment confirmation.

ADDITIONAL RESOURCES

How to Own a Payment Gateway

Payment Gateway Integration Services